Was one of your goals for 2020 to start crush your debt repayments? Even with all the crazy twists and turns 2020 has thrown our way, there is still time to make progress on your goals. The problem with paying down debt is that it can feel so overwhelming. When you see the balance you owe or your monthly payments, it can feel easier to ignore it and just move on. But, in four simple steps, you can put yourself on a path to repay your debt. Why not start today?

Step 1: Get Organized—

First, even though it is scary, you need to get organized and truly understand your debt. To do this, set aside some time on your calendar to get serious. Schedule a “Debt Meeting” with yourself. Give yourself an hour or two of uninterrupted time to organize your debt and your thoughts surrounding them.

Gather Your Information

The first step to getting organized is to get all of the information about your various debts together in one place. Using statements you’ve received and your online account information take a minute to become familiar with all of your debt.

Write Down Key information

Now that you have all of your information in one spot, write down everything you know about your debts. For each debt, be sure to include:

- Type of debt

- Interest rate

- Amount you owe

- The monthly minimum payment

- Your monthly due date

- The time until the debt is repaid if you make only the minimum payment

This information will help you understand your debt and it will let you make decisions about how to pay off your debts. I know that it can be scary to look at all of this information. But unless you understand your debts, you won’t crush them.

You can write this information down in Excel, Google Sheets, or with a pen and paper. Just be sure to keep it somewhere you can access it on your debt repayment journey.

Step 2: Find Money to Put Towards Your Debt –

Now that you are organized, it’s time to find extra money you can put towards debt repayment. In order to find extra money to crush your debt, you need to understand your spending. Take some time to review your spending over the past 6-12 months.

Using this spending, create a budget or spending plan consistent with your values. First, write down all of your fixed expenses each month. These are things like your rent or mortgage that don’t change from month to month.

Next, list out all of your variable expenses, or expenses that change from month to month. Looking at these variable expenses, what can you change? Unfortunately, to accelerate your debt repayments, you will have to cut back for a while. But you can choose what to cut. Find areas of your spending that don’t line up with your values and your goals. These are the areas to cut first. As you start trimming back, you will find extra money that you can apply towards your debt repayments.

Step 3: Prioritize Your Payments—

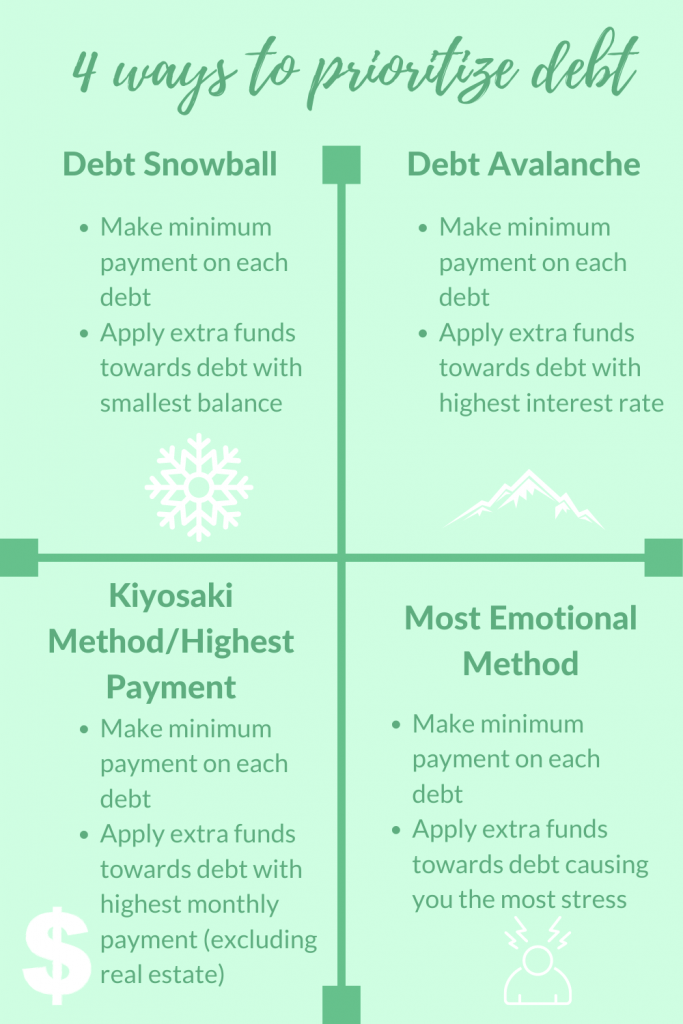

Now that you’ve found extra funds to put towards crushing your debt, it’s time to pick a repayment strategy. There are four main methods of debt repayment that you can consider.

The Debt Snowball

The debt snowball is a debt repayment strategy where first, you make the minimum payments to each of your debts. Next, you take any extra funds allocated for debt repayment and apply them to your debt with the smallest balance. You continue to pay the extra to your smallest balance until it is gone. Then pay the entire payment you were making towards to the debt with the next smallest balance. You continue to do this until you’ve crushed all your debts!

The debt snowball is great if you need a small win from the start to keep you motivated.

The Debt Avalanche

The debt avalanche is a debt repayment method where you make the minimum payment to each of your debts. Then, using the extra you have for debt repayment, you pay towards your debt with the highest interest rate. Once you’ve eliminated your highest interest rate, you apply that entire payment to the debt with the next highest rate. You do this until you have paid off all of your debts.

The debt avalanche allows you to save more money in interest over the course of your debt repayments. This is because you are paying off your debts with the highest interest rate first.

Kiyosaki Method/Highest Payment Method

With the Kiyosaki method, or the highest payment method, after making the minimum payment on each of your debts, you put all extra funds towards the debt that has the highest monthly payment (excluding real estate). You continue to apply your funds to this debt until it is gone. Then take everything you were paying towards it and apply it to the debt with the next highest payment.

This method is good because it allows you to free up more cash once your debt with the highest monthly payment is eliminated.

Most Emotional Method

Using the most emotional method, you will make the minimum payment across each of your debts each month. Then apply any extra debt repayment funds to paying off the debt that is causing you the most stress. Once you’ve crushed the debt that causes you the most stress, you can continue by paying on the next most stressful debt or you can switch to a different repayment strategy.

The most emotional method takes your well-being and stress level into consideration. Sometimes our debt comes from a bad decision or we owe family/friends money and feel guilty. Eliminating debts with these feelings associated can help you feel better about your finances as a whole.

Picking a Strategy

There is not right or wrong debt repayment strategy. It isn’t one size fits all. You know yourself and your situation better than anyone else. Keep what motivates you in mind and pick the strategy that you can see yourself sticking to. Because what ultimately matters is that you follow through and crush your debts!

Step 4: Track Your Payments –

Now that you have prioritized your debts with one of the four methods above, it’s time to start paying them down. To keep focused, track your repayments. You can track them using an app, a spreadsheet, or even pen and paper. Pick a method you will stick with. Each month, when you make a payment towards your debt, track it.

When tracking your payments, it can be helpful to organize them based on your debt repayment strategy. So, if you are using the debt snowball, your debts will be arranged from smallest balance to biggest. This can help you truly see your progress and crush your debt!

To download a free debt repayment tracker and helpful trackers, take a look at my resources.

For a more comprehensive Debt Repayment Tracker and an eBook Users Guide, visit my store.

Final Thoughts

Remember, no matter what strategy you pick or how you track, you are setting yourself up to crush your debt! As you pay off debts and start reaching goals, be sure to celebrate your wins! Celebrating small wins on your way to achieving bigger goals reinforces the good behaviors you are trying to cultivate. So, organize and prioritize your debts, track your progress, and celebrate each win as it comes! You got this! In the last four months of 2020, you can still crush your debt!