Did you know that there are five factors that affect your credit score? When I was first starting out on my personal finance journey, my credit score felt like a mystical number that appeared out of thin air. I didn’t understand how it was calculated and I wasn’t really clear on how to change or improve it. So, I did what I always do, I started researching. I quickly learned about the five factors that comprise a credit score.

But still, even after researching them and understanding the different components, I could not remember the five factors off the top of my head. When I started studying for the Accredited Financial Counselor® Exam, I finally found a way to make it stick. And I am hoping that this method works for you too!

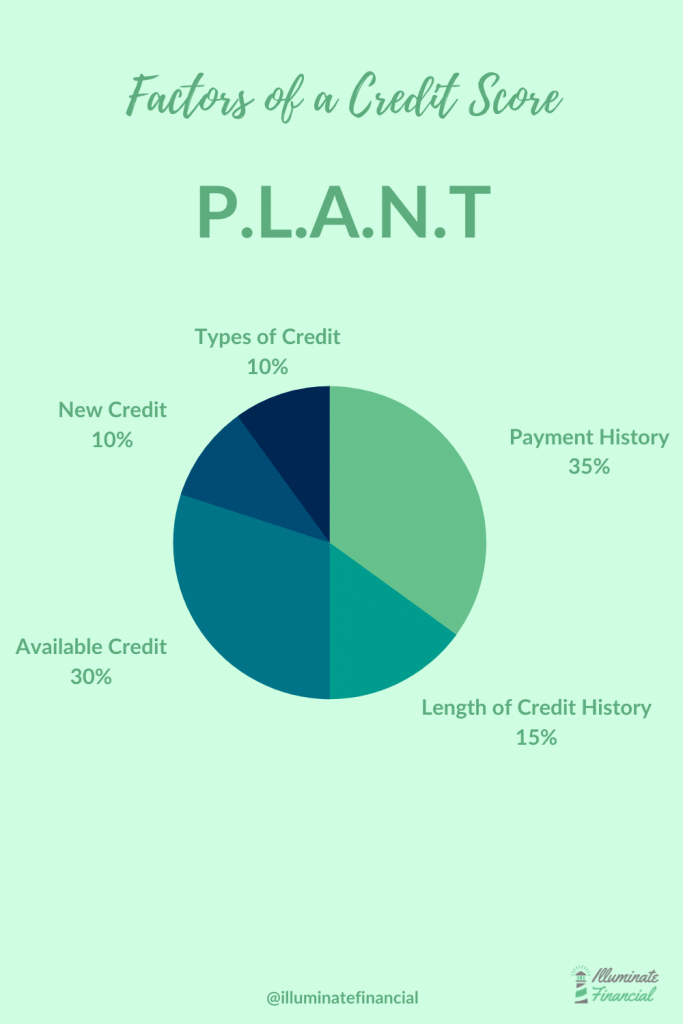

So, to remember the five factors that affect your FICO credit score, you want to P.L.A.N.T good seeds to grow good credit. This is my acronym for remembering the five factors of credit scoring. It stands for:

Payment History

Length of Credit History

Available Credit

New Credit

Types of Credit

Together, these five factors create your FICO credit score. It is important to understand each of them to build and maintain a good credit score.

Not each of the factors affects your credit score equally. Some factors like Payment History are more important and carry more weight in the scoring process. But each factor helps lenders evaluate if you are a high risk or low risk borrower. Let’s take a look at each factor in more detail to understand how lenders use them and what you can do over time to improve them.

Payment History – 35%

Your payment history accounts for 35% of your credit score. In this category, lenders will look to see if you have a track record of paying your credit account obligations on time. They consider this because a history of on-time payments often is an indicator of a responsible borrower. If you have a history of paying your credit card bills and loan payments on time, you are likely to continue to do so in the future. This means to improve your score and keep it high you always want to keep your accounts current.

This factor is the most important when calculating a credit score. So, if you are trying to rebuild your credit, focus on making each of your required monthly payments on all of your credit accounts. If you are just starting out and want to get off on the right foot, pay all of your credit accounts on time each month to create positive momentum.

Length of Credit History – 15%

The length of your credit history is 15% of your FICO score. This factor considers how long your credit history has been established. It considers three things when looking at this factor.

- How long your accounts have been established. This includes looking at how old your oldest account is, how long your newest account has existed, and the average age of all of your accounts.

- How long your specific accounts have been established.

- How long it’s been since you’ve used certain accounts.

This factor is tricky because getting a credit card is somewhat age dependent. You cannot get a credit card until you are at least 18 years old. Typically, throughout your life this category will get better on its own as you maintain credit and make payments towards any loans you borrow.

One thing to remember is that if you can avoid it you don’t want to close your oldest credit card. This can lower your score because it shrinks your credit history length.

Available Credit – 30%

Your amount of available credit accounts for 30% of your score. This category is also referred to as the amount that you owe. With this, lenders are looking to see how much you use of the credit you have available to you. This helps them determine if you are a high-risk or low-risk borrower. Typically, you want to try to use 30% or less of your available credit. For example, if you have one card with a $1,000 limit, you wouldn’t want to put more than $300 on the card.

One of the biggest myths surrounding credit cards is that you need to carry a balance on your card from month to month to increase your score. This is not true. You don’t have to maintain a balance to grow your score. You can pay it off each month and build or improve your credit.

Using more than 30% of your available credit can be a sign to lenders that you are overextending yourself. This could hurt your chances for getting more credit and using too much of your available credit over time will lower your score.

New Credit – 10%

New credit is one of the smallest factors in the FICO scoring system. This factor makes up 10% of your credit score. Lenders have found that individuals who open up lots of new credit lines/accounts in a short time are often higher risk. This is especially true for people with short credit histories. If you can, try not to open too many credit accounts too quickly. This will help keep your credit score up.

Types of Credit – 10%

Types of credit looks at the different types of credit you may have and is 10% of your FICO score. This factor considers two types of credit, revolving credit and installment credit.

Revolving credit accounts are those that provide you with a line of credit that you can use and payoff monthly, but the monthly payment varies based on how much you spent. This includes credit cards, retail store cards, and even HELOCs (home equity lines of credit).

Installment credit is a credit account that requires a fixed payment monthly until the balance is paid off in full. This type of credit account includes your mortgage, car loan, or student loans.

What lenders are looking for in this category is your ability to manage different types of credit. If you can manage your different types of credit and make on time payments, then they reason that you are a good risk and can likely manage additional credit.

Finding your Credit Score

While you can and should check your three credit reports from the different credit bureaus each year, your credit score will not show up on these reports. To check your credit report visit www.annualcreditreport.com. To find your actual credit score, you can look at Credit Karma for free. You can also use the credit score services provided by your credit card company via their website. Or, if you use Mint to create your budget you can find your credit score there as well.

Please know that when you check your credit score it does not affect your score. You also are allowed by law to collect one free copy of your credit report from Equifax, Experian, and Transunion once a year. If you aren’t making any big purchases, I recommend checking each one separately every four months. This will allow you to catch errors more readily. If you are getting ready to make a big purchase, you can check all three together to be sure they are accurate.

Final Thoughts

Remember, only charge what you can afford to pay off. If you pay off your credit card each billing period, you won’t have to pay the steep interest charges or fees. This can save you so much money each year.

You should not let your credit score define you. But building a good score can help you when you are ready to buy a house or a car. Having a good credit score can also help you rent an apartment or be charged less for insurance. It is important to understand what factors go into determining your credit score and how you can affect them to help you build a good financial foundation. It takes time to build a good credit score, but with patients, hard work, and an understanding of the system you can build a good score!

Help is Available

If you’d like to better understand the factors that affect your credit score or take steps to rebuild or improve it, I can help. Learn more about financial coaching and set up a free 30-minute ‘Get to Know You’ call today!